Eligibility Criteria

Non-MICPA members registered as ASEAN Chartered Professional Accountant (ASEAN CPA) with another participating ASEAN country, and wish to provide non-regulated professional accounting services in Myanmar may apply to be a Registered Foreign Professional Accountant (RFPA) with MICPA.

Under the ASEAN Mutual Recognition Arrangement on Accountancy Services (MRAA), a RFPA registered with MICPA (Myanmar) shall:

- Be bound by local and international codes of professional conduct in accordance with the policy on ethics and conduct established and enforced by the National Accountancy Body (NAB) / Professional Regulatory Authority (PRA) which the ASEAN CPA is registered with.

- Be bound by domestic regulations (E.g. immigration policies) of Myanmar.

- Work in collaboration with a professional accountancy firm or be employed by a company or organisation registered in Myanmar.

- Be permitted to provide accountancy services excluding signing off of independent auditor’s report and other regulated professional accountancy services that require a license from Myanmar Accountancy Council (MAC) and or any other relevant authorities in Myanmar.

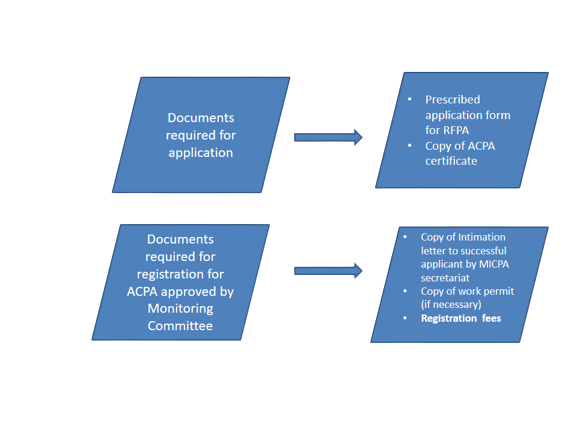

An aspiring RFPA will be required to furnish the following supporting documents at the point of application:

- Valid ASEAN CPA registration number

- Certificate of good standing from your NAB/ PRA stating that there is currently no record of any disciplinary proceedings instituted or to be instituted by your NAB/ PRA against you, dated no more than three months from the date of RFPA application. Click here for a template of the certificate of good standing for your reference.

Application

Start your RFPA application by first creating an account in the MICPA Website.

When you submit your RFPA application, you will be required to pay an application fee of US$300 (including Commercial Tax).

Please note that the application fee is non-refundable.

The application processing time is approximately twelve weeks.

Upon successful application, MICPA will inform you via email together with payment information.

The RFPA title is to be renewed annually and at an annual renewal fee of US$300 (inclusive of Commercial Tax).

For any enquiries, please email to info@micpa.org.mm.

Registration Fee : US$ 300 (including Commercial Tax)